Q1 is typically the slowest part of the calendar year in trucking. Q1 2026 was anything but, with markets white hot heading into the spring. Our latest edition takes a look at volatility as we see it through the full month of March 2026.

Spring 2026 has brought major shifts, with the flatbed market under pressure from booming construction demand—over 3,000 data center projects nationwide are driving capacity constraints. Rising fuel costs add another challenge: every $1 increase in diesel adds $0.15–$0.20 per mile in carrier costs. Broader supply-demand dynamics, empty fleet miles, and systemic changes like policy updates and AI-driven trends are reshaping the truckload landscape. Accurate forecasting is more critical than ever.

Triumph's March 2026 Truckload Market Intelligence Report helps freight professionals navigate these changes with confidence.

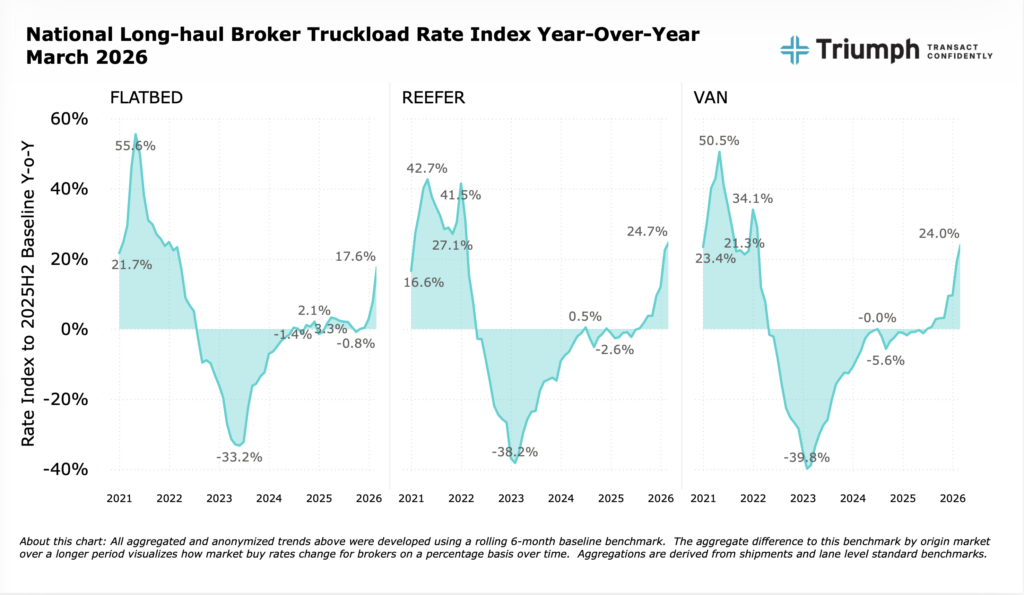

Spot Rates Rise as Routing Guides Strain

Flatbed rates jumped 13.4% month over month and 17.6% year over year. Van rates rose 3.5% month over month and 24% year over year, while reefer rates remained steady compared to February but still 24.7% higher than last year. Regional trends vary—Midwest markets see the sharpest increases, with van rates up 22% and flatbeds soaring 26%. In the Northeast and South, rate adjustments are significant, while Western markets face less pressure. As the gap between spot and contract rates narrows, securing reliable capacity grows harder, making active broker intervention essential.

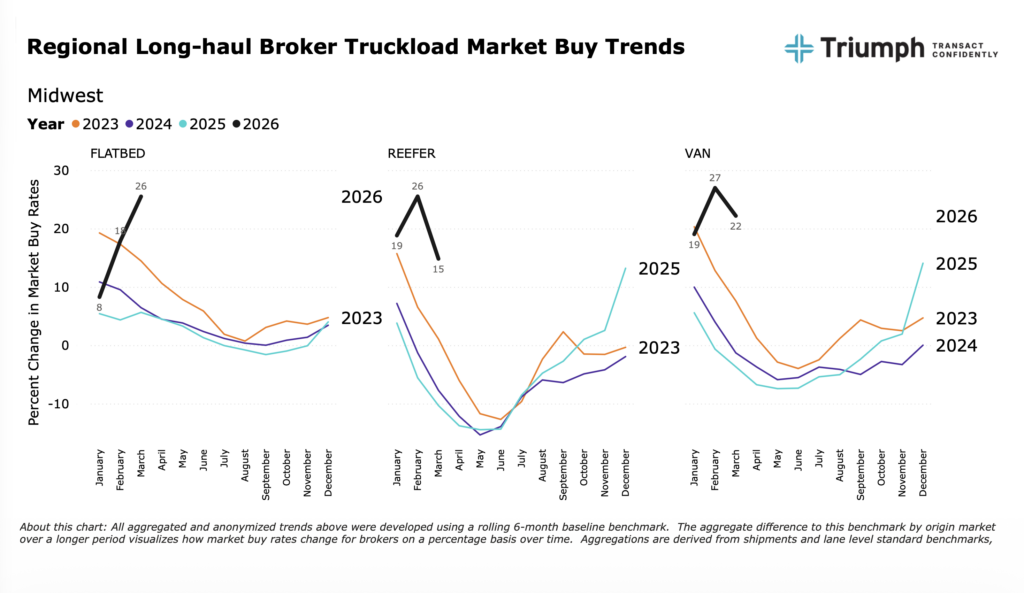

Regional Pressures Reshape Capacity

Midwest volatility leads, with van rates up 22%, reefer 15%, and flatbeds 26% above late-2025 levels. Northeast van and reefer rates remain high but are down 4–5% from February, while flatbed rates stay strong. Southern markets show cooling reefer rates alongside rising van and flatbed demand, while Western markets remain less volatile. Local nuances, delayed capacity expansion, and increasing equipment and labor demand make forecasting increasingly complex.

Midwest outbound dry van markets show early signs of tightening.

Southern markets absorb reefers rapidly during produce season.

Flatbed demand accelerates with industrial and construction growth.

Action Plan for Brokers

Adapting to these shifts requires more than monitoring data, it demands action. Brokers should revisit inflation strategies, reallocate portfolios to protect margins, and adjust shipper strategies for volatile lanes. Stay flexible, track policy and market signals, and prepare for capacity challenges and tighter shipper budgets. Using predictive data and a proactive approach will ensure you stay ahead.

The Big Picture

Systematic changes are afoot. Use forecasts with caution. Significant and material unknowns include heightened policy focus on broker-carrier liability, Iran, and the physical implications of

the AI economic revolution. Weak carrier balance sheets should rebound leading to greater demand for Class 8 equipment and labor. Capacity expansion may be delayed as a result of the

systemic changes ahead. Shipper budgets will be impacted most as the market balance is clearly favoring carriers. Price trends will decipher the market correction - stay tuned!

At Triumph, we see these trends unfold daily. What’s your outlook for capacity this spring? Share your thoughts in the comments, and subscribe to our newsletter for more insights.

Intelligence products and services are offered by TBK Bank, SSB, Member FDIC,d/b/a Triumph