After COVID, we thought we had seen it all. Then came 2026.

Early data show that DOT Blitz week was unusually strong this year. However, unlike prior cycles 2026 appears to be different. Results from the Triumph Intelligence network are staggering on a week-over-week basis across volume, margin, and rate.

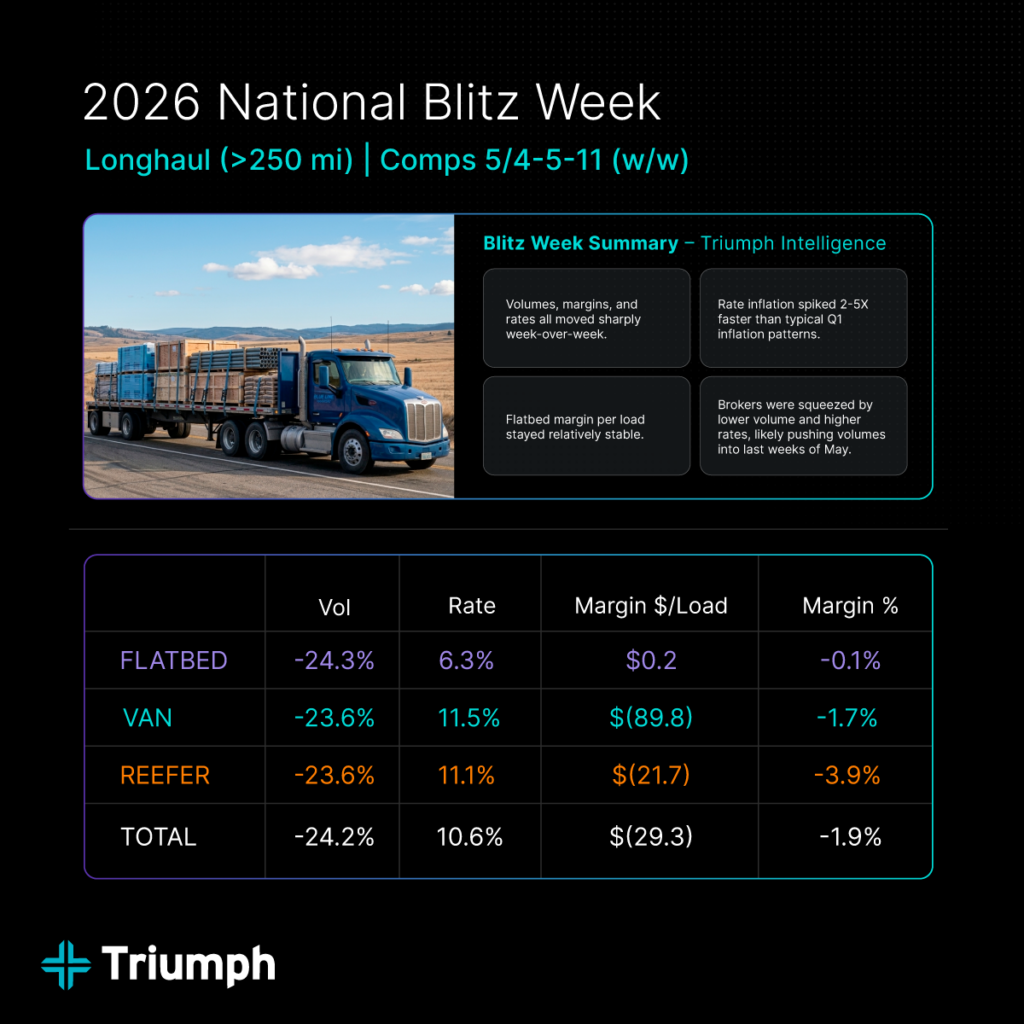

Blitz Week: Quick Summary

- Volumes, margins, and rates all moved sharply week over week.

- Rate inflation spiked faster than typical seasonal patterns.

- Flatbed margin per load stayed relatively stable.

- Brokers were squeezed by less capacity on higher rates.

Flatbed margin per load was largely unaffected, but the rate inflation measured on a weekly basis exceeded the monthly spikes seen during COVID—our last major rate shock. Brokers faced lower volume, reduced total margin, and significantly higher rates. Anecdotal reports also suggest that the inflationary impact of DOT Blitz week continued beyond the week of 5/11. Given the sharp drop in volumes, it is likely that demand has been pushed into the second half of May.

As the broader supply constraint persists beyond May and carrier balance sheets recover, the next material pressure point in the trucking market is likely to be capacity bottlenecks in equipment availability and the supply of qualified drivers as drivers move in and out of the industry. Industry reporting indicates that some new Class 8 equipment is currently scheduled for delivery in December, with year-over-year order activity roughly doubling and near-term first-half 2026 build slots nearing full utilization. In tighter market conditions, backlogs can extend materially, with lead times exceeding over a year during extreme periods.

As carrier gross revenue continues to improve, demand for experienced drivers is likely to increase—especially as spot rate trends show no sign of easing, route guides fail, and mini-bids become a weekly occurrence for shippers. Hiring an experienced driver typically takes 4 to 12 weeks; while onboarding new entrants can take 3 to 6 months. Cost per hire generally ranges from $5,000 to $12,000 and can exceed $20,000 or more when training, advertising, and productivity losses are included. High turnover, regulatory requirements, and sustained competition for skilled drivers continue to constrain net driver additions, even when recruiting activity increases.

In response, large carriers are relying on a mix of retention-focused compensation and benefits, accelerated recruiting technology, improved route planning, apprenticeship programs, and selective acquisitions to support growth. Many experienced drivers who have left trucking after years of suppressed rates may return to the industry—but only if rates provide a meaningful incentive. In short, the market is prioritizing trusted relationships, an element that was diminished as rapid digitization pushed logistics toward a swipe-left, swipe-right model over the past decade. Carriers need trusted drivers, shippers need trusted carriers and brokers.

As the industry continues to evolve through the lens of liability and safety, measured fleet expansion appears increasingly likely. Key indicators to watch include Class 8 order and production data, ISM Manufacturing as a signal of underlying demand, and any developments related to broker and carrier revocations. Broadly speaking, carrier bonus programs have historically signaled the beginning of a peak in rates. With so much capacity leaking out of the system, I expect the next expansionary cycle to take much longer to work through.